In the intricate web of global finance, the mechanisms of support between developed and emerging economies have evolved significantly. Among the most critical, yet often understated, tools are central bank currency swaps and strategic market interventions. These instruments have moved from the periphery of economic discourse to the center stage, especially during periods of global financial stress. They represent not just technical financial operations, but a profound commitment to international monetary stability.

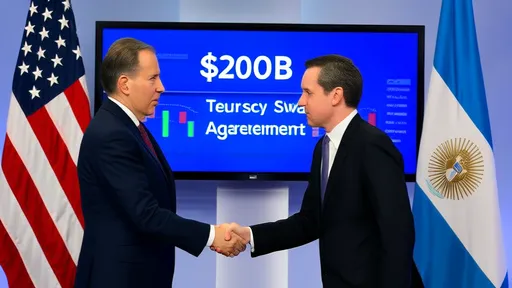

The concept of a currency swap between central banks is, in essence, a lifeline. It is an agreement where two institutions exchange currencies for a predetermined period, with an agreement to reverse the transaction at a later date. For an emerging market, grappling with sudden capital flight or a crashing currency, access to a swap line with a major central bank like the Federal Reserve or the European Central Bank can be the difference between a managed downturn and a full-blown crisis. It provides immediate access to hard currency, most commonly the US dollar, which is the lifeblood of international trade and finance.

Historically, such swap lines were a closed club, predominantly among the central banks of major advanced economies. The 2008 global financial crisis, however, marked a paradigm shift. The Fed, recognizing the systemic risk posed by a global dollar shortage, extended temporary swap lines to several key emerging economies, including Brazil, Mexico, and South Korea. This was a landmark moment. It signaled that the financial stability of large emerging markets was inextricably linked to the health of the core developed world. The global financial system was acknowledged as a single, interconnected organism.

Beyond the immediate crisis-fighting role, these swap arrangements carry a powerful psychological weight. The mere announcement that a central bank in an emerging economy has secured a swap line with the Fed or the ECB can calm jittery markets. It acts as a stamp of approval, a signal to international investors that the country has a credible backstop. This can stem capital outflows and stabilize the local currency without a single dollar actually being drawn upon. It is a tool of confidence as much as it is a tool of liquidity.

Market interventions, on the other hand, are the more visible hand of central bank policy. When a currency comes under speculative attack or experiences excessive volatility, the central bank may step directly into the foreign exchange market. This typically involves selling its reserves of foreign currency, like dollars or euros, to buy its own domestic currency. The goal is straightforward: to increase the supply of the foreign currency and increase demand for the local one, thereby propping up its value.

For emerging markets, however, this tool is a double-edged sword. A country like Turkey or Argentina might burn through billions of dollars in reserves in a matter of weeks fighting a market trend. If the intervention fails, the country is left with depleted reserves and a still-weak currency, eroding investor confidence further. This is where the synergy with swap lines becomes apparent. A swap line effectively bolsters a country's war chest, providing it with the ammunition to conduct more credible and sustained market interventions. It tells speculators that the central bank has the firepower to defend its currency, making a successful defense more likely.

The geopolitical dimension of this financial support cannot be overlooked. The extension of a currency swap line is not a purely technocratic decision. It is a deeply political act that strengthens alliances and creates spheres of financial influence. When the Fed provides a swap line, it reinforces the centrality of the US dollar and deepens the financial integration of the recipient country with the United States. Similarly, China has been actively promoting its own currency swap network through the People's Bank of China, as part of its broader strategy to internationalize the renminbi and build an alternative financial architecture. This creates a new layer of geopolitical competition, where financial stability is used as a tool of statecraft.

Critics, however, voice significant concerns. They argue that this safety net can create a dangerous moral hazard. Knowing that a backstop from a major central bank might be available, governments in emerging economies might be tempted to delay necessary but painful economic reforms. They might persist with loose fiscal policies or maintain artificially high exchange rates, under the assumption that they will be bailed out during a crisis. This can store up even larger problems for the future, as underlying economic weaknesses are papered over rather than addressed.

Furthermore, the selective nature of this support raises questions of fairness and systemic risk. Why do some emerging economies receive swap lines while others, often more vulnerable ones, do not? The criteria are often opaque, based on the systemic importance of the country's financial system to the core economies. This creates a two-tiered system where a handful of "too-big-to-fail" emerging markets enjoy a privileged safety net, while smaller nations are left to fend for themselves, potentially exacerbating global inequalities.

The future landscape of this financial support is likely to be shaped by the lessons of the past decade and the rise of new economic powers. The network of bilateral swap agreements is becoming denser and more multipolar. While the dollar's dominance remains unchallenged for now, the euro, the yen, and increasingly the renminbi are becoming more prominent in these arrangements. There is also ongoing discussion about strengthening multilateral safety nets, such as increasing the lending capacity of the International Monetary Fund, to provide a more universal and rules-based form of support.

In conclusion, the interplay between currency swaps and market interventions represents a sophisticated and evolving framework for financial support from developed to emerging economies. It is a system built on the recognition of shared risk in a globalized world. These tools provide crucial breathing room for policymakers and can prevent localized financial shocks from spiraling into global contagion. Yet, they are not a panacea. They come with geopolitical strings attached and carry the risk of fostering complacency. The ultimate challenge for the international community is to harness these powerful tools to build a more resilient and equitable global financial system, one where stability is not a privilege for a select few, but a foundation for shared prosperity.

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By Ryan Martin/Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025

By /Oct 11, 2025